The thought of being without health insurance can be very scary.

Many of our friends work in jobs they hate, just to obtain health insurance for themselves and their families. We were among those ranks until just recently. Several months ago, I remember having a heart to heart with my younger sister about retiring early. I was really struggling with my job at this point (September 2018) and ready to pull the trigger on retiring early, but health insurance was the sticking point.

Mr. Sunshine and I are both in our 50’s. We are both runner’s, training regularly, with normal BMI, normal blood pressure and normal cholesterol. Mr. Sunshine has no health problems and takes no medications (except vitamins, fish oil, etc.). I have trouble with hot flashes (menopause) and depression (recent death of my 22 year old son), taking medication for both of these conditions. The medication for my hot flashes costs $140 per month by itself.

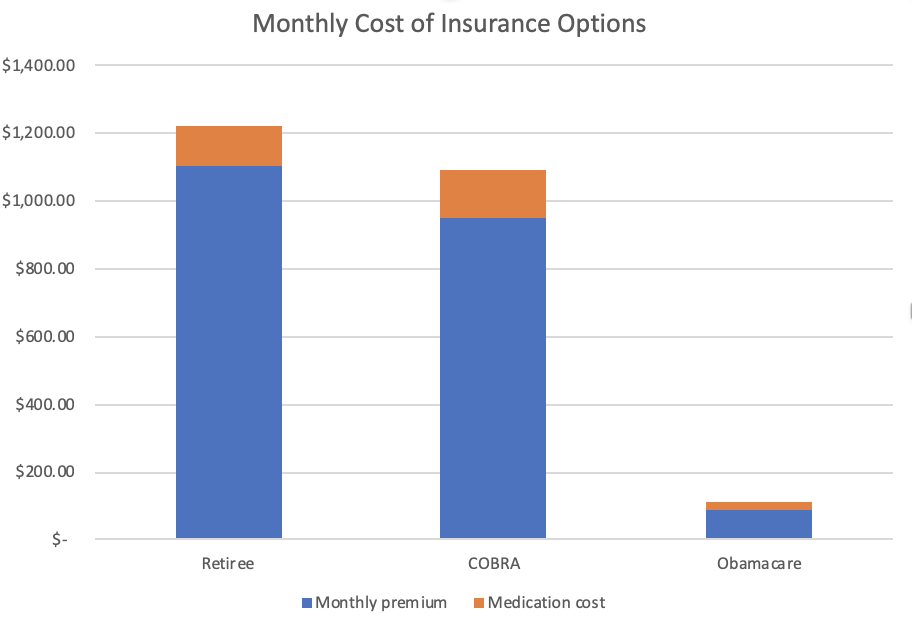

As a retiree from my previous job I have the ability to purchase health insurance at cost ($1100 per month for both of us). We also have the ability to use COBRA from my most recent job ($950 per month for both of us). These costs just seem astronomical, given that we use very little health care.

Having heard about the low cost of Obamacare, I found the marketplace website and looked up the costs. Ouch! They were more expensive than my other options. Then, I found the key. The health care subsidies are based upon income, not on net worth. Why does this matter?

A person can have one million dollars in the bank and still qualify for subsidies! No Way! But it is true!

We have a net worth of $XXX,XXX but live on an annual budget of about $36,000 per year. We can live this low because we have no debt and no mortgage. We live frugally. After playing with the numbers, it seemed to us that $24,000 of yearly income gave us the best subsidies. The difference in income will come from our savings.

This means that despite our high net worth, we can qualify for subsidies and low cost health insurance! Early retirement here we come. I felt like I was let out of prison – freedom.

January 2019, I changed my retirement plans to the maximum allowed to reduce our taxable income. I have access to a 403B, a 457, and a HSA. My last paycheck was March 31 with a gross taxable YTD income of $5875, well under the $24,000 income limit that I set for us.

So yes, April 1 (April Fools’ Day) was my first day of freedom – seems fitting. Fingers crossed that my insurance plan works!

Today, I sat down and applied for health insurance through the marketplace at healthcare.gov. I chose a silver plan with the following benefits:

- Deductible $675 individual/ $1350 family

- Out of pocket max $675 individual/ $1350 family

- Primary care visits – no charge

- Preventative care services – no charge

- Specialist visits without referral – $5 copay

- Emergency room visits – no charge after deductible

- Diagnostic testing and imaging – no charge after deductible

- Drugs: Generic at no charge, preferred $25, non preferred – no charge after deductible. (My medication will be $25 per month with this plan).

My high deductible plan thru my employer was $142 per month. In addition I paid $140 per month for my medication. Minimal monthly cost thus = $280. (We are on a high deductible plan, so we pay all expenses except preventative until we reach $7500).

Our new plan will be $88 per month, with the cost of my medication at $25 per month our new monthly total will be $113 per month with primary care visits at no charge. This is a tremendous boost to our ability to be able to retire early and slow down to enjoy life. Our insurance cost is less and it covers more than my employer plan.

I filed our application today, we have a life event that qualifies us to obtain insurance mid year – my job loss – otherwise we would have to wait until open enrollment.

A few possible problems to over come yet. I have to show proof of prior coverage and loss of employment. I called our HR department and obtained my COBRA letter to upload for proof as suggested on the site. Now we wait to see if this is accepted. One more large problem – our insurance if approved will not become effective until the beginning of the following month (May 1). This leaves us without coverage for the month of April.

Our plan – because we have more than 30 days to decide if we take the COBRA insurance – we can get insurance retroactive to April 1 if necessary. Wow, this is really a bonus. If we need coverage in the month of April (an expensive trip to ER, etc.) then we can elect coverage and it will go back and cover the expense – wouldn’t it be nice if all insurance worked like this. Pay premiums only if you need the coverage 🙂

You can see if you would qualify for subsidies at this link: https://www.healthcare.gov/lower-costs/qualifying-for-lower-costs/

and also at

https://www.kff.org/interactive/subsidy-calculator/

Finally, remember that your taxable gross income is under your control. You can shift your income to tax advantaged accounts (pre-tax) while working before retiring early. We had enough money in our high interest savings account for living expenses for these first few months of the year and could afford a nearly zero paycheck. Now we must make sure that we do not go over $24,000 of income for the year. This is completely under our control. We will be doing some Roth conversions later in the year but will need to be wary of this cap to avoid having to repay the subsidy amounts.

It is still yet to be seen how easy the insurance plan is to use. I have checked to make sure our primary care provider and local hospital are within network, but beyond that – will report back in the future.

3 thoughts on “Health Insurance for early retirement”